Overview

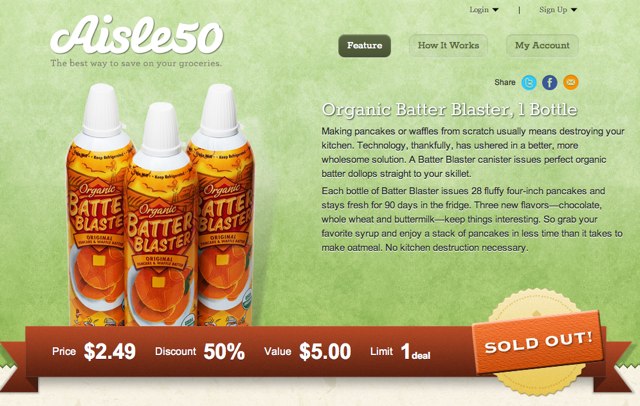

Aisle50 was a Chicago-based digital grocery promotions platform that let CPG manufacturers fund deep discounts — often 50% or more — on their products, which consumers purchased online and redeemed in-store via their grocery loyalty card.Founded in 2010 and backed by Y Combinator, August Capital, Ron Conway, and Yuri Milner, the company raised approximately $6 million across two rounds and built a genuinely differentiated product with strong per-transaction metrics.

Its core thesis — that CPG promotional spending would migrate from print newspaper inserts to digital channels — was directionally correct.But Aisle50 was ultimately constrained by the grocery industry's structural resistance to adopting new technology at scale.

The company never landed a national retail partner, leaving it dependent on a patchwork of regional chains that could not generate the consumer density needed to attract major CPG budgets.Eighteen months after its Series A, Aisle50 was acqui-hired by Groupon in February 2015 — the very company it had spent years differentiating itself from — and the product did not survive the transition.

Founding Story

Christopher Steiner came to Aisle50 with an unusual background for a startup founder: seven years as a senior staff writer at Forbes covering technology.[1] That journalism career gave him a sharp analytical lens on market transitions, but it also meant he was entering the grocery and CPG industry without operational experience in either. His co-founder Riley Scott brought complementary skills, and a third co-founder, George Korsnick, joined as CTO — though Korsnick received almost no press coverage and his tenure at the company is not well documented.[2]

The company was originally named GrocerGoose before rebranding to Aisle50,[3] a change that suggests an early rethinking of how the product should be positioned. The founding date is itself disputed: Steiner's personal website cites 2010, while the YC database and some press sources suggest 2011.[1] The company was headquartered at 648 West Randolph Street in Chicago's West Loop.[4]

The founding insight was straightforward: the grocery industry had spent decades driving consumer demand through Free Standing Inserts (FSIs) — the coupon booklets stuffed inside Sunday newspapers. That channel was expensive, wasteful, and increasingly ineffective as newspaper readership declined. As Steiner put it at the time: "the grocery industry has been built around using major promotions to build consumer demand for ages," and Aisle50 positioned itself as the digital evolution of that system — one where a manufacturer could spotlight a single product without competing ads on the adjacent page.[5]

The team entered Y Combinator's Summer 2011 batch and debuted at Demo Day in August 2011 with a pitch that the press immediately shorthandled as "Groupon for groceries."[6] The framing was useful for investor comprehension but slightly misleading — the structural differences from Groupon were precisely what made Aisle50's model interesting.

For Pro Subscribers

Unlock the full Aisle50 teardown

Read the complete post-mortem, the rebuild playbook, and the exact reasons Aisle50 is still worth studying now.